.png)

Introduction

In traditional financial markets, market makers have existed for decades, providing liquidity and facilitating trades to allow markets to operate efficiently. However, the world of crypto has introduced a new twist to the role of market makers, with multiple methods and models to choose from.

All token issuers will ask themselves the same question: What is the right market making model for our token and why?

This article covers an overview of market making and the various models used across the crypto landscape. It also highlights the critical questions and details token issuers should understand before their token launch.

What is market making?

Market making is a crucial component of the financial ecosystem, enabling the dynamic and active trading of billions worth of assets every day. At its core, the role of a market maker is to provide liquidity in the market by continually buying and selling assets. The crypto market is known for its volatility, but what is less well-known is the critical role played by market makers. Without market makers, the crypto market would struggle to function effectively. Market makers ensure traders can always buy or sell tokens at a fair price, allowing projects to grow, attract new members, and contribute effectively to their respective ecosystems.

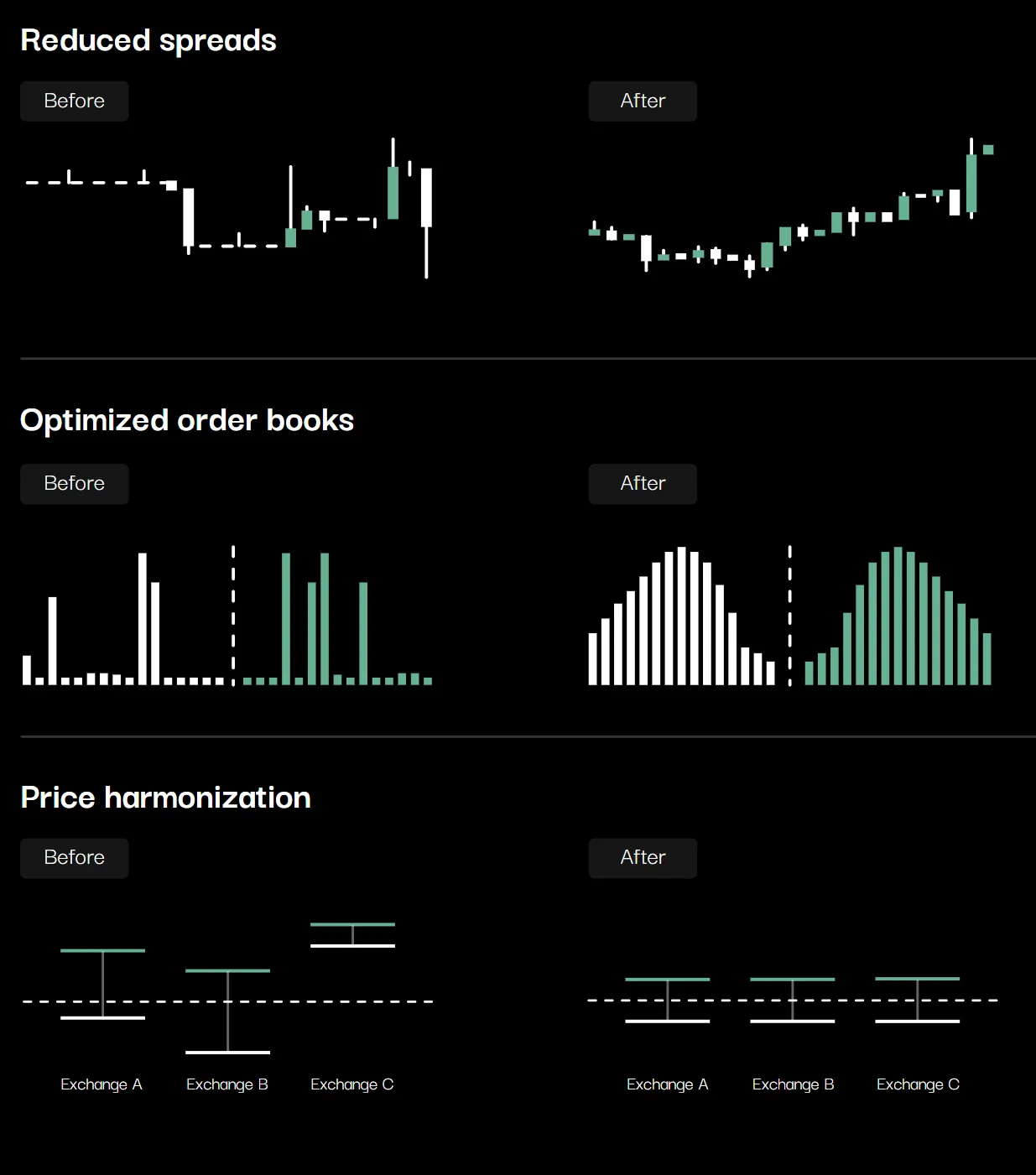

Market makers provide the necessary liquidity for smooth trading. They do this by constantly offering to buy and sell cryptocurrencies, which ensures there are always enough orders in the market for traders to match. In turn, this reduces volatility, narrows the bid-ask spread and promotes a more efficient trading environment.

Why does crypto market making matter?

Here are three key reasons:

- Venue fragmentation: crypto markets span across centralized exchanges (CEXs), decentralized exchanges (DEXs), and liquidity pools. Market makers help ensure prices are harmonized across different venues, capturing eventual arbitrages across centralized and decentralized exchanges.

- Price stability: by constantly providing buy and sell orders, market makers help to maintain price stability 24/7/365. This is crucial in the crypto world, which can be highly volatile.

- Market efficiency: market makers help to ensure that the price of a cryptocurrency on an exchange accurately reflects its market value. This is done by reducing the bid-ask spread, which is the difference between the highest price that a buyer is willing to pay for an asset and the lowest price that a seller is willing to accept.

Crypto market making is evolving rapidly. As more institutional investors enter the digital asset landscape, there is a growing demand for more sophisticated market making services.

Centralized exchanges (CEXs) often require projects to engage professional market makers to ensure liquidity and efficient trading at all times. At the same time, the rise of decentralized finance (DeFi) and automated market makers (AMMs) is changing the landscape. Decentralized Exchanges (DEXs), like Uniswap, use a mechanism to execute buy or sell orders via a liquidity pool, removing the need for traditional market makers.

However, while AMMs offer some advantages, they also have limitations, such as inefficient markets, the potential for impermanent loss, slippage, and susceptibility to price manipulation. Due to the strong developments in Layer 2’s efficiency over the last years, many DEXs are also moving towards using order books to match the usability and power of CEXs. As a result, there is still a need for professional market makers who can navigate the complexities of the crypto market and maintain liquidity on both centralized and decentralized exchanges.

The crypto market also remains largely unregulated, often allowing large market makers and exchanges to set their terms freely. This can lead to situations where market makers trade against the projects' interests for their own benefit, especially in volatile market conditions.

Different Market Making Models for Token Issuers

Within the crypto landscape, there are two primary market making models: the loan and call option model and the market making as a service (retainer) model. Each model has distinct capital requirements, strategy designation, exchange coverage, KPIs, risk profiles, and remuneration characteristics. While it’s impossible to say one model is definitively better than the other, selecting between the two models depends on the characteristics and objectives of each token issuer.

Loan / Call Model

In a loan/call option model, the token issuer loans the market maker tokens for trading inventory (typically quoted as a percentage of total supply) and issues a call option on the loan. The market maker can choose to return the tokens or exercise the call option if the market price is higher than the previously agreed-upon strike price.

The market maker defines the trading strategy and is compensated through the call option and gamma trading of the option.

Key characteristics:

- Inventory for market making activities: Token issuer provides token inventory via a loan to the market maker, quoted as % of total supply. Market maker deploys balance sheet on buy side

- Capital risk: Market maker assumes risk of capital because it provides the cash/equivalent assets

- Liquidity strategy: Market maker defines the trading strategy

- Exchange selection: Market maker selects which exchanges to support and the levels of liquidity

- Remuneration: Market Maker is compensated through call option and gamma trading of the option.

Retainer Model (Market Making as a Service)

In the retainer model, the token issuer loans the market maker its token for trading inventory in addition to the quote currency (e.g., USDC). The token issuer pays the market maker a monthly fee for the trading activity and the trading infrastructure, and at the end of the contract, the market maker returns the full loan.

The token issuer defines the trading strategy alongside the market maker.

Key characteristics:

- Inventory for market making activities: Token issuer provides token inventory and the quote currency as a loan to the market maker.

- Capital risk: The token issuer assumes risk of capital

- Liquidity strategy: The token issuer defines the trading strategy alongside the market maker

- Exchange selection: The token issuer selects on which exchanges the Market Maker will be trading and the levels of liquidity

- Remuneration: The token issuer pays the market maker a monthly fee.

Measuring Market Making Performance

- Bid-ask spread: a tight bid-ask spread is the primary metric to monitor when working with a market maker. Note, it’s important to also recognize the depth at the bid-ask spread. For example, bid-ask spread might be 5bps for a high liquidity alt coin but there might only be a few hundred in liquidity. A wider bid-ask spread at 30bps with $100k in depth is a healthier indication for traders.

- Guaranteed uptime: Market makers need to quote prices all the time. However, market volatility and trading infrastructure issues can cause a trading downturn. Generally, market makers should have the infrastructure to allow for > 95% uptime.

- Latency: speed of trading infrastructure is critical when selecting a market maker to ensure responsive and efficient trading with different exchange integrations.

- Market maker responsiveness: Crypto markets are ever-changing, so market makers must be agile and adapt to evolving market conditions. Unlike traditional markets, crypto markets trade 24/7, so having infrastructure and teams worldwide is crucial.

- Reporting: Trust and transparency are essential when working with a market maker. Ensure the market maker offers real-time dashboards or regular reports to monitor trading activity, depth, spreads, market share, PnL, and other important KPIs.

Red Flags:

- The market maker is guaranteeing that the token will reach a certain price point: The goal of Market Making is to create liquid market, and while this can help the token grow in price due to a more favorable trading environment, there are also illegal activities directly aimed at increasing the price of the token that can be considered market manipulation, such as Spoofing.

- Lack of compliance and regulation frameworks: The absence of AML & KYB processes should be seen as a red flag. Regulated Market Makers are required by law to have clients go through these processes.

Lack of transparency: A lack of transparency is never a good sign and should always raise a red flag. Nowadays some Market Makers will also be able to provide you with a live dashboard that allows you to keep track of the activities at all times.

Helpful Questions to Ask a Market Maker

- How many traders and engineers does the firm have? (This can be indicative how well they will actually be able to hit their KPIs)

- What kind of technology and infrastructure do you use for market making? Is it proprietary?

- What market making/trading strategies do you employ?

- Can you explain your approach to minimizing spreads and slippage?

- How transparent are you about your trading activities and performance metrics?

- What kind of reporting and analytics do you provide to token issuers? How often will we receive these reports?

- How do you handle potential conflicts of interest that may arise from market making activities?

- How do you ensure compliance with regulatory requirements in different jurisdictions?

- What key performance indicators (KPIs) will we use to measure the success of our market-making agreement?

Conclusion

By understanding the role of a market maker and comparing popular models, token issuers can make more informed decisions about managing liquidity and trading for their tokens. In any case, token issuers are paying for a service. The retainer model charges a set fee, while the loan/call model can sacrifice some of the token's potential upside.

Ultimately, token projects should carefully evaluate these pros and cons based on their objectives, risk tolerance, and the current market environment to choose the most appropriate strategy for their market-making requirements.